Sign In

Welcome! Sign In to personalize your Cat.com experience

If you already have an existing account with another Cat App, you can use the same account to sign in here

Register Now

One Account. All of Cat.

Your Caterpillar account is the single account you use to log in to select services and applications we offer. Shop for parts and machines online, manage your fleet, go mobile, and more.

Account Information

Site Settings

Security

Managing Risks, Reaping Rewards through CHP and CCHP

Securing success in combined heat and power using reciprocating engines

John C.Y. Lee

Caterpillar Asia Pte. Ltd., Electric Power Division

Asia Territory Manager

Michael A. Devine

Caterpillar, Electric Power Division

Gas Product Marketing Manager

Steven J. Szymanski

Caterpillar Financial Services Asia Pte. Ltd.

International Sales Manager for Electric Power, Asia-Pacific

September 2013

ABSTRACT

The world today offers a wealth of opportunity for combined heat and power (CHP) installations. CHP using reciprocating gas-fueled engine-generator sets can support a wide variety of industrial processes, as well as district heating and cooling systems. It contributes reliable, clean electricity for captive use or export to the grid while providing a high-quality heat source. It is an excellent option for large operations, especially in areas where central utility power is subject to power quality issues or has frequent outages.

Engine-driven CHP and combined cooling, heat and power (CCHP) can achieve total thermal efficiencies to 90 percent, or in some cases even higher. It can bring substantial savings on electricity costs and rapid return on investment. It can be even more profitable when using low-cost “opportunity fuels,” such as methane from agricultural or food processing wastes, landfills, or wastewater treatment plant digesters.

INTRODUCTION

The prospect of self-generating profitable heat and power should not blind potential owners to the risks of CHP projects. Like any generating facility, CHP plants require proper capital investments and effective long-term operation and maintenance regimens. The key to a successful project is to recognize all risks and allocate each one to the party best equipped to manage it. For a typical CHP project, those risks include:

• Fuel (reliability, quality and price)

• Revenue (energy sales or savings)

• Technology (equipment track record and performance/efficiency)

• Operations (uptime, ease and availability of operation and maintenance)

• Permitting (environmental, noise, and others)

• Construction (schedule, plant performance, cost)

• Credit (financing and debt repayment)

• Insurance (physical damage and public liability)

• Inflation (for both revenue and expenses)

Risks are best managed through contracts. The project owner, lender, equipment supplier, contractors and other parties must assemble a functional, reliable solution that meets financial and performance objectives.

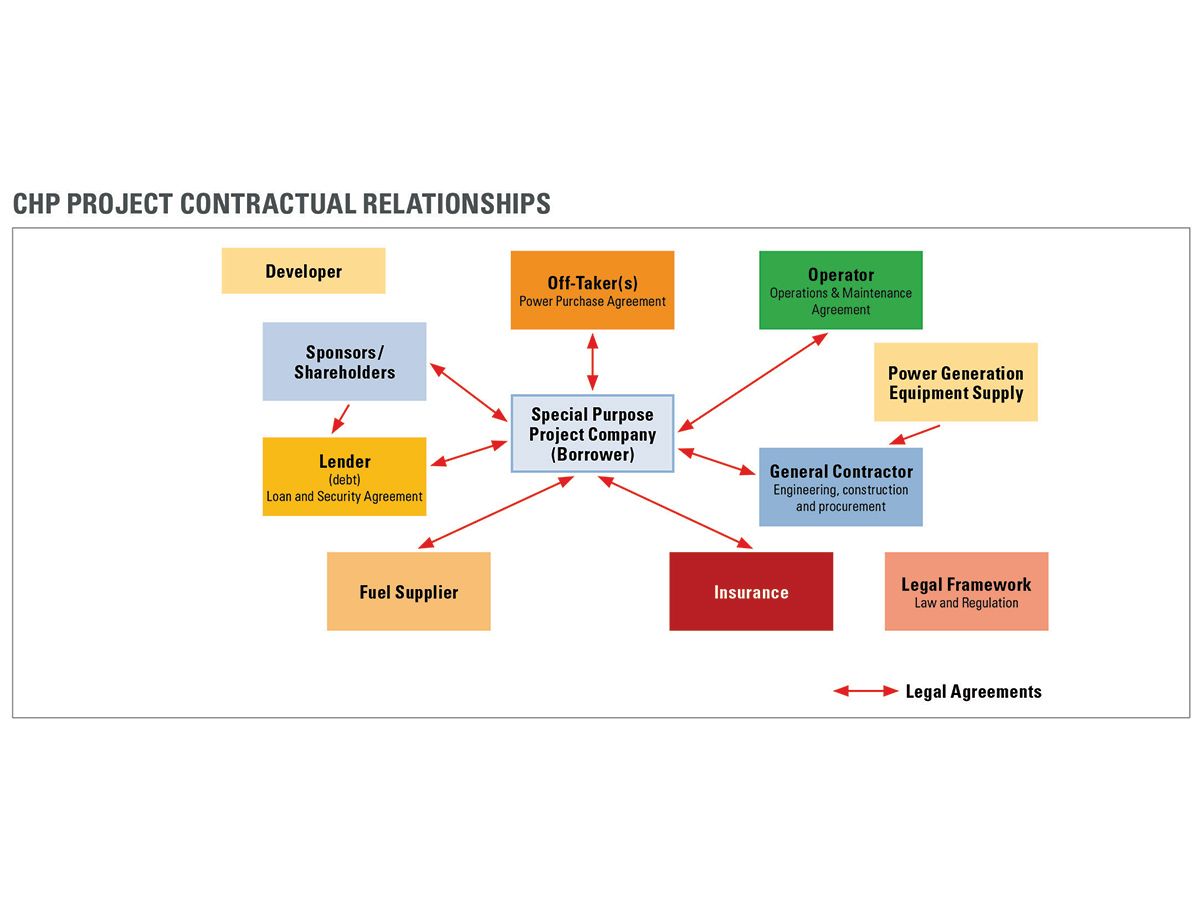

Figure 1: Complex interplay between multiple project needs and multiple players

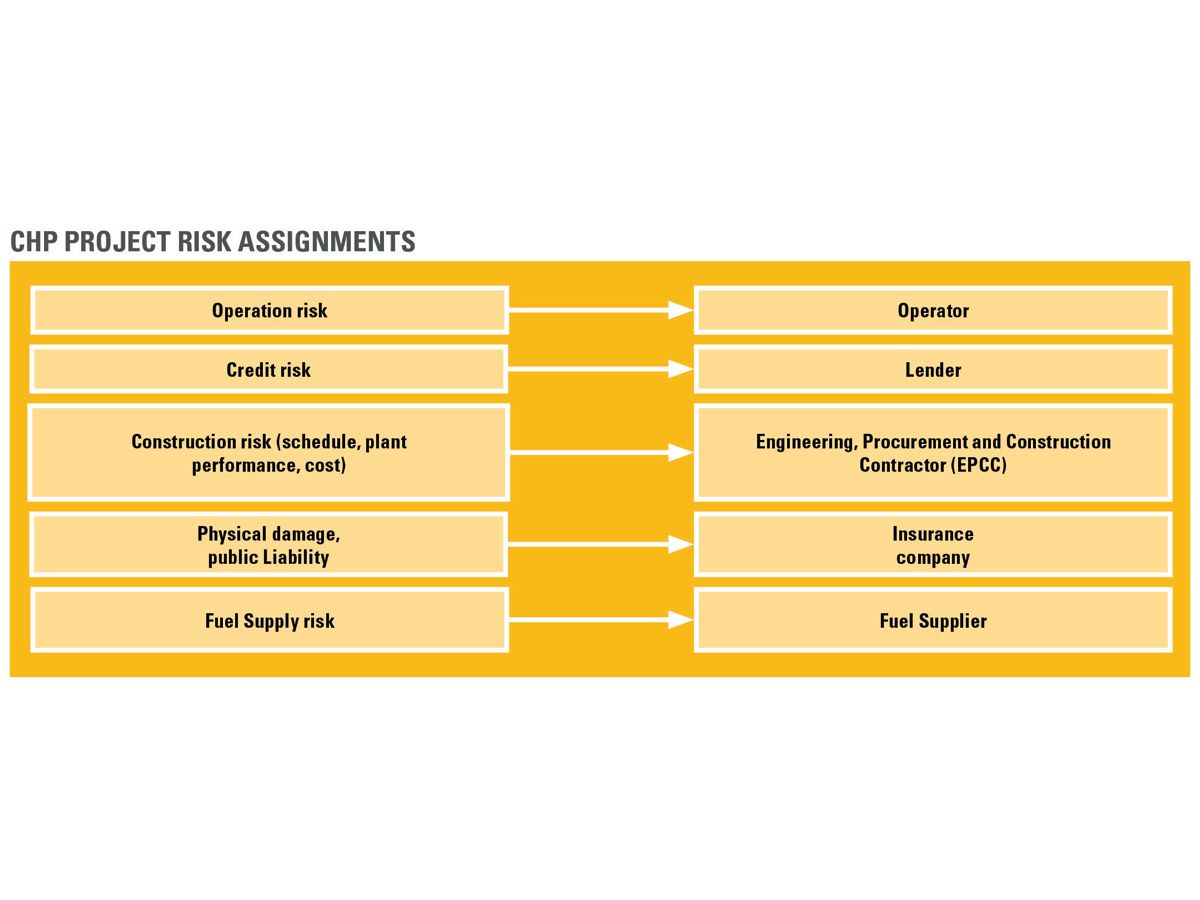

Figure 2: Assigning risks to the party best qualified to manage it

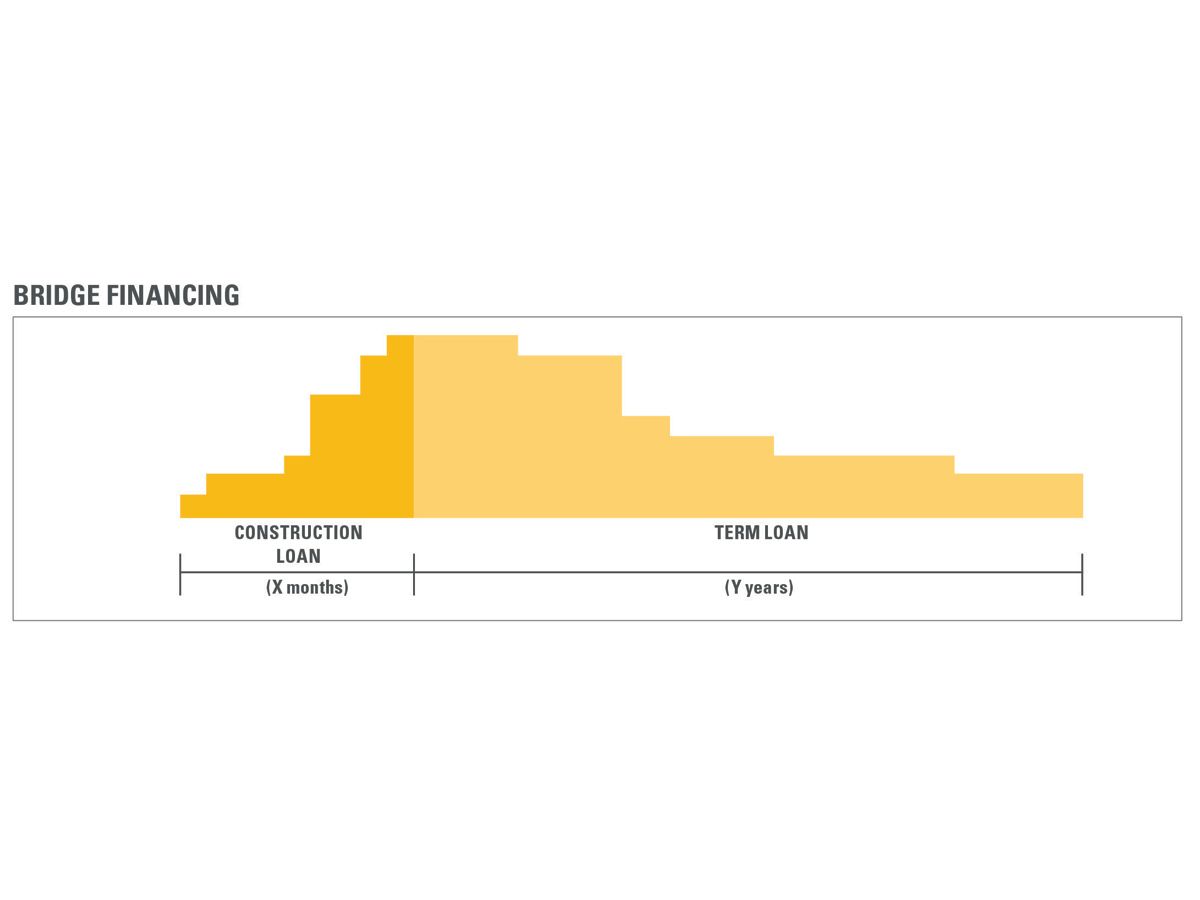

Figure 3: Construction vs. Term Loan Timeline

Chart 1: Applications for Recovered Engine Heat

Chart 2: How availability affects the performance of a CHP project

Chart 3: How availability affects the performance of a CHP project

TAPPING THE POTENTIAL OF CHP

CHP has growth potential because economic, social and political trends work in its favor – to varying degrees depending on the condition in the host country. Some national, provincial and state governments offer incentives for CHP that can include partial

investment grants, favorable structured feed-in tariffs (FITs), duty-free capital equipment importation and value-added tax exemptions, all designed to promote cleaner renewable fuels and reductions in greenhouse gas emissions, especially from coal-fired central power plants. In addition, programs for rural electrification in some nations encourage development of small-scale energy projects in outlying areas, where CHP can be especially beneficial.

While local power reliability can be a key driver of CHP or CCHP, the decision to proceed with a project generally comes down to economics: Will savings on energy costs and revenue from electricity generated provide adequate return on the investment in the equipment and its operation? A key factor that can favor gasfueled CHP is spark spread – the difference in cost per equivalent unit of energy between commercial natural gas prices and electricity rates. The outlook is most favorable where the spark spread is large: fuel prices relatively low and electricity cost relatively high. CHP also can prosper where:

• The system will operate with a high electrical and heat and /or chilling load factor

• Electric and thermal loads coincide during a typical day

• The site requires high reliability and power quality

• The CHP system can double as a standby power source

• Low emissions are important

PUTTING HEAT TO WORK

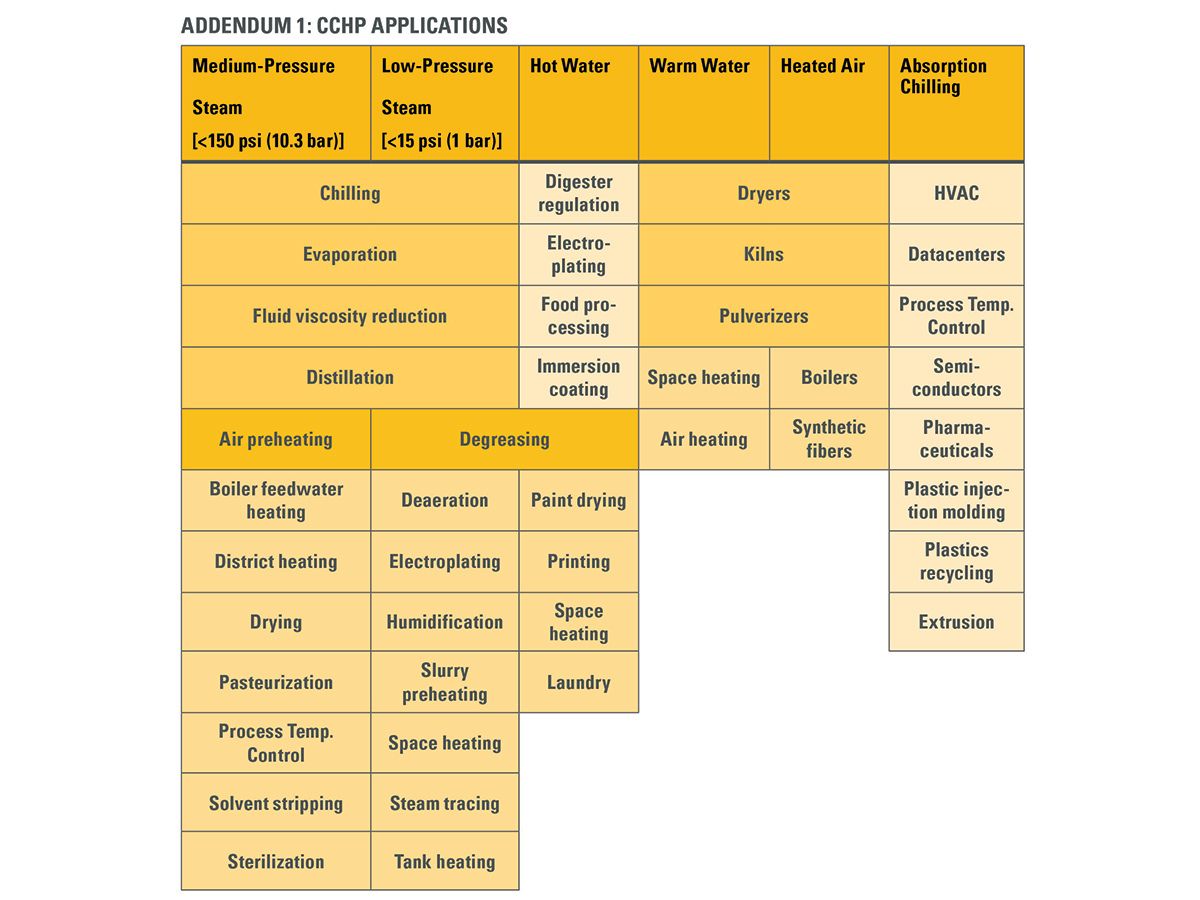

With today’s technology, heat from a CHP plant is a valuable and versatile resource (see Addendum 1). Modern lean-burn gas-fueled reciprocating engines are rich sources of heat.

Engine exhaust provides by far the highest temperatures and the greatest heat output. At a typical temperature of about 460°C (860°F), exhaust can generate intermediate-pressure steam for purposes like boiler feedwater heating, and low-pressure steam for sterilization, pasteurization, space heating, tank heating, humidification, and absorption chilling. Supplemental firing with natural gas can increase exhaust heat output to produce steam at greater volumes and pressures for many industrial uses. Beneficial heat can also be extracted from the engine jacket water, with lower quality heat available from the oil cooler (when not on the jacket water circuit) and aftercooler.

Hot water and steam are the classical engine outputs in CHP systems, but they are not the only ones: They can be converted to other forms to suit additional purposes. Steam or hot water can be passed through heat exchangers to create hot air to feed equipment such as kilns and dryers. Steam, hot water or exhaust can be fed to absorption chillers to produce chilled water for space or process cooling. Heat-recovery systems can be configured to deploy some heat for water and steam production and the balance to absorption chillers. Alternatively, systems can produce space heat in winter and air conditioning in summer.

Beyond heat recovery, carbon dioxide is a usable byproduct of power generation: Engine exhaust rich in CO² can be cleaned in a catalytic reduction unit, cooled and fed to a process. In greenhouses, for example, CO² helps crops grow faster, improving yields by 10 to 20 percent. Exhaust can also provide a low-cost source of CO² for industrial applications or even for carbonation in soft drinks. Taking efficiency to the ultimate level, a single generator set can deliver electricity, space or process heating, space or process cooling, and CO² – a concept known as quad-generation.

Cogeneration is not limited to highly engineered systems that maximize production of both electricity and heat: Simple and well-conceived heat recovery can improve the economics of many electric power projects with only a modest additional investment. Almost any application that entails roughly 1,000 or more annual operating hours offers potential for economical heat recovery. The only firm requirement is that the value of heat recovered outweighs the added cost of the heat-recovery and control mechanisms.

KNOWING THE RISKS

Delivering the benefits of CHP means responsibly addressing the risks inherent in building and operating the facilities. For one thing, projects tend to be relatively small – generally 1 to 10 MW – yet may have “soft costs” (legal and development fees) similar to those of much larger projects. Energy and its environmental considerations typically fall outside the core competencies of the project owners, and equity capital may be in short supply, despite project risks that demand higher levels of it. This and other factors make effective risk management essential.

Fuel supply risk

A CHP project is unlikely to succeed if the long-term fuel supply is unpredictable or the fuel quality is uncertain. Project economics typically depend on a specific quantity of energy produced, and a resulting target generator set capacity factor. A project based on, say, 95 percent capacity factor will surely fail if the fuel supply is often interrupted or curtailed, or if poor fuel quality keeps the equipment from operating at full rated output.

This concern is magnified where a project will rely on a non-traditional fuel, such as biogas from a landfill or food processing waste. In such cases, the project developer needs an ironclad, long-term contract with a feedstock supplier and should avoid situations that would allow the supplier to entertain offers from other feedstock users. For projects fueled by utility natural gas, the developer needs a contract that provides reasonable certainty about the future fuel price. In either case, a lender will typically require an agreement that ensures suitable fuel supply and pricing for two years beyond the loan repayment term.

Revenue risk

Similarly, if selling power or heat, a CHP project needs a long-term energy purchase agreement that binds the energy purchaser to a specific volume of kilowatt-hours, therms, or both, at agreed-upon prices for the duration of the project financing term. Short-term purchase agreements or buy-as-needed contracts are generally not considered financeable unless a strong guarantor agrees to pay the loan regardless whether the electricity can be sold. A suitable contract typically includes a mandatory purchase (take-or-pay) obligation: The energy buyer cannot default on a purchase for any reason, including, for example, a malfunction of a transmissional line or other facility within the buyer’s control that stops the flow of energy. As in fuel supply agreements, an energy purchase agreement typically needs to extend two years beyond the loan repayment term.

Technology risk

Not all generating technologies are designed, manufactured, and serviced with equal quality. It is incumbent on the project owner to select prime movers, generators, heat recovery systems and ancillary equipment with an eye toward a track record of performance in similar applications. While initial installed cost per kilowatt-hour matters to project success, proven reliability matters a great deal more (see Addendum 2). As part of due diligence, a project owner should ask all prospective equipment suppliers to offer references and data on successful projects of similar size and type, using a similar fuel.

Operations risk

The best energy generating technology’s performance is only as good as the ongoing support it receives in the field. Improper maintenance or poor operating practices can lead to unplanned downtime that puts project financial results in jeopardy. Project owners should expect an equipment supplier to have built a substantial product support infrastructure in-country. This can include remote monitoring and diagnostics, on-demand technical support, fully qualified service technicians able to respond in less than 24 hours, and a local parts stocking and distribution network that ensures prompt delivery of genuine original-equipment replacement parts. Major expenses such as engine overhauls should be budgeted. Most project lenders will require a reserve account for major maintenance to be established and funded over time to cover these periodic costs. An attractive option is to enter a complete operations and maintenance agreement with the equipment supplier that covers all planned service at an annual fixed cost. This generally will negate the need for the project owner to establish a reserve account for major maintenance.

Permitting risk

Each market has its own permitting regimen. Permits may be needed for environmental compliance, factory operations, construction, air space, noise, forestry, and a variety of other requirements. The permitting authorities may be both national and local. It is essential to understand the permit processes and allocate appropriate time to permitting. Some countries have streamlined permitting processes for small renewable energy projects, but it is a common misconception that environmental permitting for such projects will be simple.

Construction risk

The engineering, procurement and construction (EPC) phase of a CHP project requires an experienced contractor and proven equipment and component suppliers. Critical guarantees of milestones, such as project completion date, net electrical and thermal output, and the fuel heat rate based on local fuel parameters, need to be secured up front. Liquidated damages should be payable for missing any guaranteed parameter and should be sufficient to compensate for the resulting cost or loss of energy output.

For example, liquidated damages for failure to meet the completion date should be enough to cover the additional interest cost during construction. Liquidated damages for heat rate should compensate the owner for the net present value of additional fuel that will be consumed for the duration of the contract. In addition, the project owner needs to have enough equity in reserve to cover a cost overrun and still complete the project.

Typically, lenders require a lump sum EPC contract that provides a complete “wrap” of the construction of the project. Payment and performance bonds (or comparable standby letters of credit) may also be required by lenders.

Credit risk

Financing is a key hurdle for any CHP project. The two basic forms of financing carry substantially different risks for both lender and project owner.

Balance sheet financing requires the company that owns the project to pledge, in effect, its “full faith and credit” toward it. Assuming the owner has a strong balance sheet, financing in this scenario should be relatively quick and easy to obtain: The lender derives comfort in the form of the company’s track record, assets, cash flow and profitability. That means lower risk and therefore generally a lower interest rate. However, some companies prefer not to carry energy projects on their balance sheet, operating them instead as separate business entities or contracting with third parties.

In such scenarios, non-recourse project financing is used. Here, no proven, stable parent company stands behind the payment obligations of the project: Its financial viability depends solely on the project’s own revenue, profit and cash flow. Given the challenges of retrieving installed engines and ancillaries and the customized nature of electric power projects, even the equipment itself offers the lender little by way of collateral. Due diligence becomes much more stringent: Is a long-term power purchase agreement in place? How reliable is the supply of feedstock for fuel? Is there a supply contract in place? If so, for how long? Is the project developer experienced in the energy sector or with power generation? Because the review process is more involved and the risks greater, the interest rate and development costs generally will be higher.

Essentially, from a lender’s perspective, the difference between balance sheet and project financing is like the difference between investing in a blue-chip company versus a startup company.

Insurance risk

The entire project must be adequately insured against physical damage and public liability for accidents, property damage or personal injury. It should also be insured against lost revenue from business interruption, such as from a storm, flood or fire.

Inflation risk

The financial model needs to include an adequate inflation factor covering both revenues and expenses. This should include inflation in construction capital costs as well as the long-term inflation that may affect operating costs, such as replacement parts, labor, rents and general expenses.

MANAGING RISKS EFFECTIVELY

All these risks can create a complex interplay between multiple project needs and multiple players (see Figure 1). Project financing depends on a legal and binding framework of agreements covering all parties. Every relationship represents a risk that needs managing. In general, the more players, the greater the risks: One party’s failure to perform can undermine an entire project.

The way to manage risks is through written contracts. These contracts must assign each risk to the party best qualified to manage it (see Figure 2). All these contracts must work together without mismatches or conflicts. There may be several iterations of the contracts before all of the relationships and responsibilities between the parties are properly integrated.

PROJECT ECONOMICS

After all risks are considered, the success of a CHP project comes down to economic performance, in particular cash flow. Under project financing, lenders typically require a project to generate 1.5 times the cash needed to cover the debt obligation – after taxes and all expenses – during each year of the project loan. A project lender will require a detailed financial model that clearly shows all assumptions and follows generally accepted accounting principles to portray the project economics accurately. The model should be userfriendly to allow the lender to review various “what-if” scenarios and test the strengths and weaknesses of the project economics.

Revenue side

Base revenue amounts to the value of the net kilowatt-hours and therms produced and sold. That in turn depends upon:

- Availability. Revenue is lost anytime the CHP equipment does not operate, such as during maintenance and repairs, or at times when the fuel supply is reduced or interrupted.

- Load factor. Ideally, the generating equipment operates at full rated load; a fuel supply shortfall or a decline in fuel quality will restrict output and revenue.

- Derates. Overheating, high ambient temperature and high altitude may keep the generating equipment from achieving its nameplate capacity rating.

Revenue also includes incentives such as government grants and tax breaks and utility-sponsored rebates or special renewable energy tariffs.

Expense side

On the opposite side of the ledger fall owning and operating expenses:

- Fuel. This typically is the largest item at 60 to 80 percent of project operating cost (unless an “opportunity fuel” is available).

- Capital expense. This includes the cost of generating and heat recovery equipment, fuel production, interest during construction, legal and development costs, funding for cost overruns, interest rate, loan amortization, and management of the project schedule.

- Operating expense. This includes staffing, replacement components, supplies and consumables, engine/generator set and facility maintenance and repairs, periodic engine overhauls, and taxes.

From the total of these costs, a thermal credit is deducted – the economic value of the recoverable heat.

Maintenance and repairs are an expense over which project owners have substantial control. Predictive maintenance can help extend generator set service and overhaul intervals and reduce service costs by up to 15 percent. Good predictive practices include regular oil analysis to help optimize service intervals; monitoring of trends like valve recession, oil consumption and emissions to fine-tune overhaul schedules; and use of tools like vibration analysis and infrared thermography to detect trouble before failures happen.

Any economic analysis needs to consider potential revenue stream risks (decline in gas volume or quality, power line outages that interrupt power sales) and upsides (more and better-quality gas than expected, favorable renegotiation of the energy purchase agreement or fuel supply pricing, greater-then-expected equipment availability).

PUTTING IT ALL TOGETHER

One way to simplify a CHP project is to work with a partner well qualified to manage a number of the basic risks – such as an engine-generator manufacturer with a diverse technology portfolio, a well-developed dealer network and a strong financing arm. That partner can bring to bear:

- A variety of generating technologies in a broad range of power ratings to suit many applications. This can include engines designed specifically to operate on low-energy biofuels, and engines custom engineered for local ambient conditions, altitude, fuel quality, and site-specific performance objectives.

- In-country dealerships with broad experience in operating and maintaining power generation equipment and with locally based service technicians. Such dealers can offer a wide range of service programs, from basic planned maintenance and overhauls to comprehensive long-term service agreements.

- Dealerships able to manage whole-project engineering, procurement and construction and supply all engines and generators, plus transformers, heat recovery equipment, switchgear, gas treatment systems, and other ancillary equipment.

- Diverse financing capability that includes intimate knowledge of the special needs of power projects in general and CHP projects in particular. This can include expertise in financing small projects ($5 million or less); knowledge of development processes, project economics, and incentive programs in each country; capacity to finance entire projects rather than equipment only; and flexible financing approaches to suit specific customer needs.

An especially valuable attribute in a partner is the ability to provide construction financing – a form of bridge financing while the project is under construction and not yet producing cash flow. Upon substantial completion of the project, the construction loan is converted into long-term financing (see Figure 3).

Moving forward

CHP projects offer major opportunities to generate profits, enhance energy efficiency, and improve sustainability in the Asia-Pacific region. These are favorable times for municipalize and industrial facility operators to explore the full potential of producing electricity, heat, and cooling from a single source of fuel.

ADDENDUM 1

CCHP APPLICATIONS (see Chart 1)

ADDENDUM 2

IT’S ABOUT KILOWATTS – AND HOURS

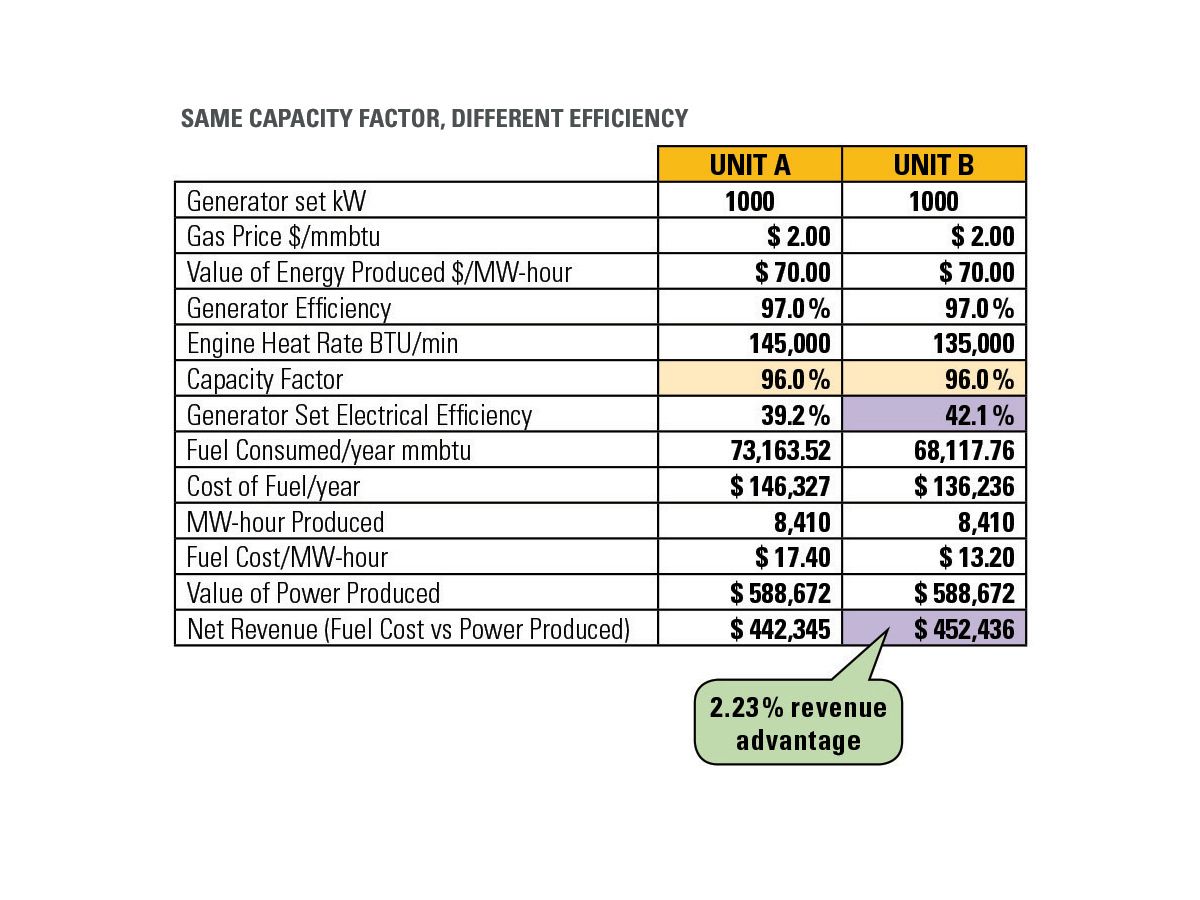

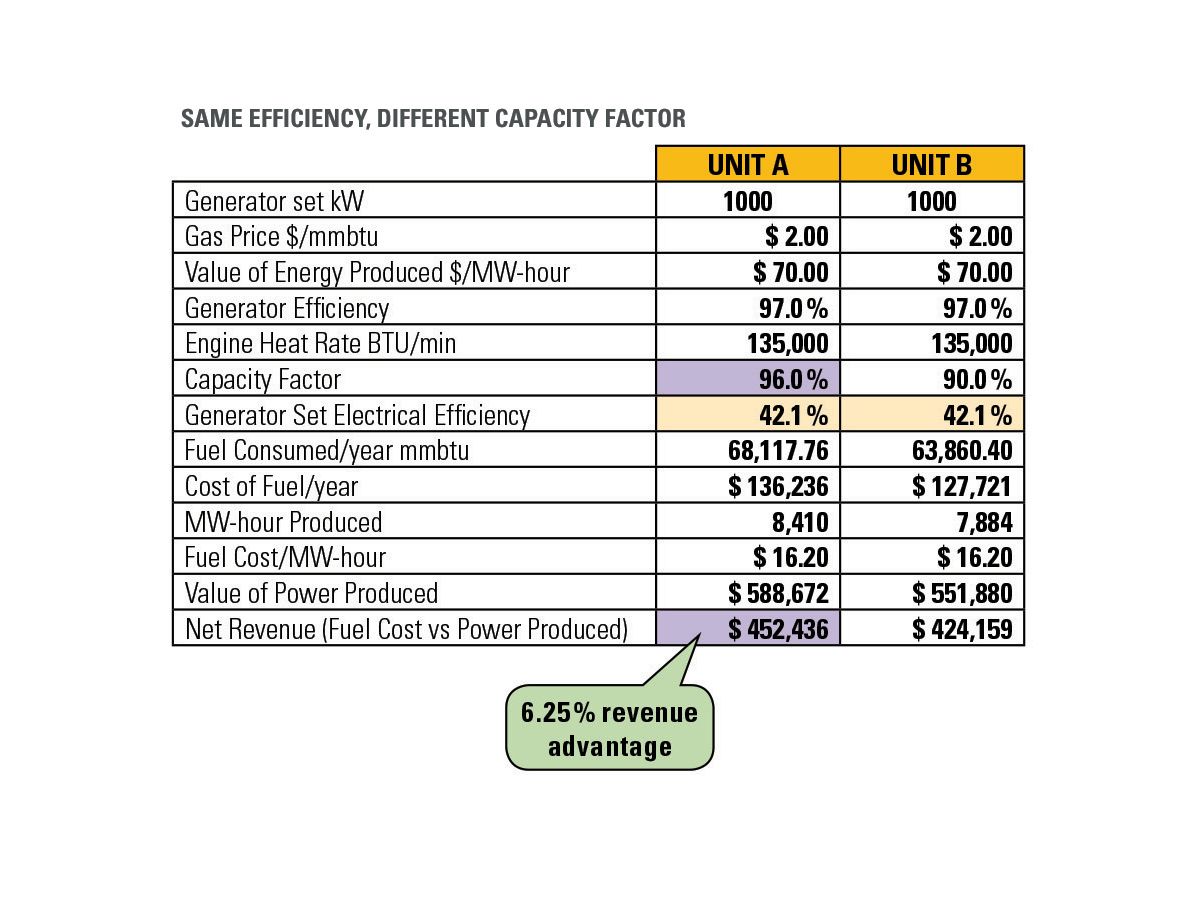

In assessing the performance of a combined heat and power project, the equipment’s efficiency is important – but not nearly as important as its availability (uptime). Simply stated, anytime the generating equipment is offline, it produces zero revenue. Its kilowatts of capacity are devalued when its hours of operation are reduced.

A simple scenario illustrates the tradeoff between generator set electrical efficiency and availability, as they affect revenue. Assume two 1 MW units, an electricity sale price of $70 per MWh, and a fuel production cost of US$1.90 / GJ (US$2 /MM Btu).

Now assume that both units operate at 96 percent availability, but that Unit A is 39 percent efficient while Unit B is 42 percent efficient. In that scenario, the more efficient Unit B has a 2.2 percent net revenue advantage (see Chart 2).

Now for the same two units, assume that electrical efficiency is the same at 42.1 percent, but that Unit A’s availability is 90 percent and Unit B’s is 96 percent. In this scenario, the more available Unit B has a 6.25 percent revenue advantage (see Chart 3).

ADDENDUM 3

CHP PROJECT ECONOMICS

Every CHP project is different: No single, simple financial model applies because fuel volume and quality, owners’ objectives, local thermal and power requirements, and other parameters vary greatly. However, here are a few general rules of thumb:

Typical capital expense

Capital cost depends on the gas production, power generating thermal production technologies and the plant design. Estimates for 2013 for a project in Asia are:

- For a typical 2 MW power plant, one can estimate capital investment of US$1 million

- If heat or absorption chilling is required, then additional investment up to US$0.5 million may be required

- Balance of plant can run up to US$1 million depending on complexity and standards

- Permitting and other soft cost can be upwards of US$0.25 million

Project economics depend on whether the revenue from sale of power and heat is adequate to support the capital and operating costs and still provide a reasonable cash flow. A more capitalintensive technology may require a longer loan repayment term to generate enough cash flow. If the longer loan term is not supported by an even longer-term power purchase agreement, then the project may not be viable.

Financing terms

- Typical loan term: minimum of 7 years (power purchase agreement must be 2 years longer)

- Typical loan amount: 70 percent of total project capital cost

- Interest during construction: Accrued into the loan principal

- Interest rate: LIBOR plus a margin, dependent on the project risk analysis. The variable rate can be converted to a fixed rate. Local currency may also be available.

- Fees: Legal and lender’s engineer fees payable up front as billed

- Debt service reserve: Equal to six months of principal plus interest

- Cash management account with an agent bank: Collect payments from the power purchaser, pay expenses and loan payments, then issue dividends.

Results

- Debt service coverage ratio not less than 1.5:1 for the duration of the loan

- Equity internal rate of return greater than 25 percent

- Simple payback less than 5 years